Ticker Reports for November 6th

What a Trump Win Looks Like for the Market Now and Into 2025

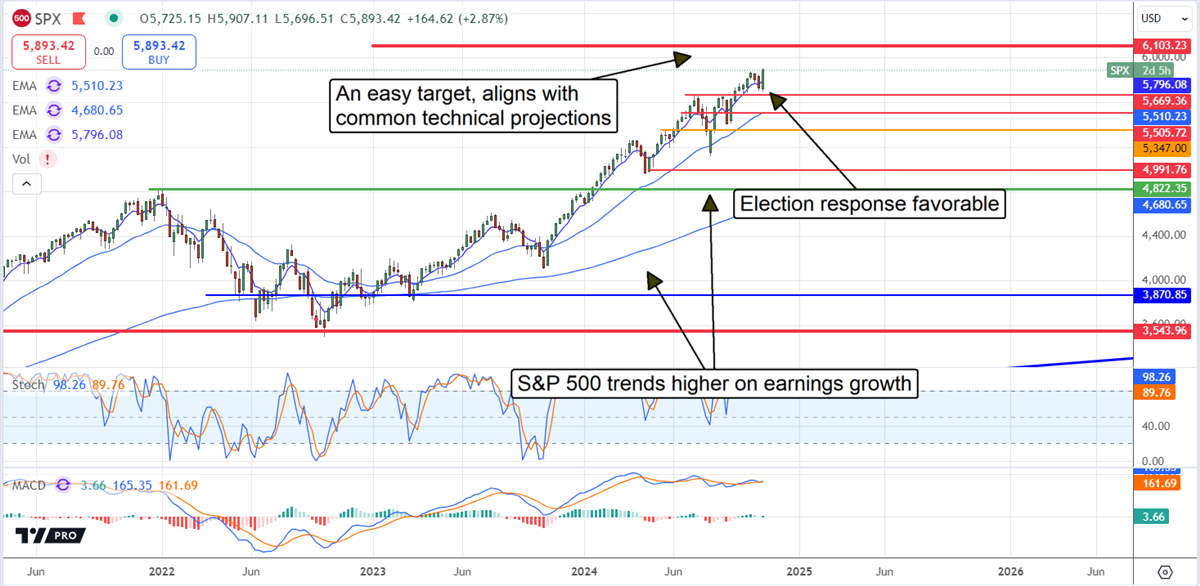

As surprising as it may be, Donald Trump won a second term in office. One of few to do so non-consecutively, his 2nd term has long-lasting repercussions for the market. If history is to be used as a guide, those repercussions will be good for stocks. Looking at the S&P 500 (NYSEARCA: SPY) starting the week of November 16th, 2016, just after his first victory, through the results of elections in 2020, investors stand to win big. The S&P 500 gained roughly 70% then and was tracking toward new highs in Q1 2020, just before COVID-19 hit the proverbial fan.

The S&P 500 Advanced 70% After Trump’s First Win

Trump’s first term brought market gains, but also volatility; it did not move higher in a straight line. Drivers of volatility included his trade war with China, which is still technically underway. Many but not all of the restrictions put in place by the Trump administration are gone, and some new ones exist. Trump will likely hammer down on this and other policies, aiding the reshoring of industries ranging from consumer goods to semiconductors.

Another driver for the market is Trump’s business-friendly policies. In the first term, he lowered taxes, easing headwinds for businesses, and he will do the same this term. Extending the cuts enacted by the 2017 Tax Cuts and Jobs Act is a priority on the agenda. Some of those will expire at the end of the year, and the president-elect wants to build on them. Additionally, he plans to cut taxes at all levels, including taxes on tips, social security, and overtime, which will significantly boost consumer spending power.

Trump Was Good for Labor Markets

Healthy labor markets and improving consumer conditions are hallmarks of the first administration. The labor data trended favorably going into the term, and those trends strengthened as the term progressed. Unemployment hit the lowest levels since the housing crisis, job creation was trending near historical highs, and job openings were rising, leading to a high quit rate. Quit rates are important because they indicate high employee confidence and reflect healthy consumer spending power.

Today's labor data is down significantly from 2022 to 2023, but the decline is relative. The peaks in 2022 and 2023 were driven by the COVID-rebound and stimulus spending, normalizing to align with the healthy levels in late 2019 and early 2020. The new Trump administration will likely support labor market health and help it to sustain growth for the next four years.

Trump and the Fed: Inflation May Be Sticky

There is FOMC and inflation risk, but it is out of his control. However, the Fed is on track to lower rates periodically in 2025, easing the headwinds put in place since 2022, which is favorable to the Trump agenda. The consensus is for the base rate to fall to 4% or lower by the end of 2025, ultimately creating tailwinds in the housing and consumer markets.

Strong labor markets and spending should sustain the outlook for S&P 500 revenue and earnings growth, potentially leading to an analyst upgrade cycle and an upwardly trending index. The risk is that improving economics will sustain inflation and keep rates well above the 2% target and interest rates above historical norms if less restrictive than now.

Earnings Growth and Capital Returns Sustains the S&P 500 Uptrend

The outlook for S&P 500 earnings has diminished from highs set earlier in 2024 but remains robust. The index earnings grew in Q3 2024, and the consensus forecasts growth will accelerate to the low-double-digit range in Q4 and sustain at those levels in 2025. Trump’s election will likely create a dual tailwind for those figures, making it easier for businesses to operate and consumers to spend. In that world, the stock market rally will likely broaden and include more than a few sectors.

The outlook for the S&P 500 is to reach 6,000 by the end of the year. The market is trending higher on momentum, earnings growth, and the expectation for easing interest rate pressure, and the uptrend can be sustained indefinitely in this scenario because of capital returns. The S&P 500 is on track to pay over $600 billion in dividends next year, up roughly 5% from 2024, and is expected to sustain the pace of growth, if not accelerate it, each year under Trump.

Gold at $2,600... But This Stock Gives You More for Under $20

Gold just soared over $2,600 an ounce.

But what if I told you there's a way to get exposure to MORE than an ounce of gold... for less than $20?

Russell 2000 Surge Post-Election: How to Play the Small-Cap Pop

The presidential election for the United States, probably one of the most awaited events and catalysts in the stock market for the year, is now over and Donald Trump is the President-Elect. The market and different participants have now taken on their views as a conclusion from the results, and it looks like most cyclical names will be in play for investors to consider.

Not only are these cyclical names made up of consumer discretionary stocks, but a particular mix is to be considered in the small-cap niche of the market. As the market opens for the first day of post-election results, investors see the iShares Russell 2000 ETF (NYSEARCA: IWM) and its 5% rally as a sign of confidence from the group. On a relative basis, small caps seem to be one of the best places to be.

However, it’s not all sunshine and rainbows, as the iShares 20+ Year Treasury Bond ETF (NASDAQ: TLT) keeps selling off to push higher bond yields. These yields act like gravity on small-cap stocks; the higher they are, the harder they make it for smaller companies to take off. However, the ETF holds a few exceptions, like Sprouts Farmers Market Inc. (NASDAQ: SFM), Mueller Industries Inc. (NYSE: MLI), and even HealthEquity Inc. (NASDAQ: HQY).

Why Small-Cap Stocks Are Rallying Post-Election—and Key Risks to Watch Out For

Markets consider a Trump victory to be bullish for the economy, and small businesses are the ones to lead the way into whatever expansion the economy may have moving forward. Relative to the S&P 500 and its 2% rally, the small-cap ETF is giving investors something to consider as it rallies by more than double.

Despite the initial bullish reaction, investors need to consider rising bond yields as a fair warning. Higher yields will raise the cost of capital and financing, making it harder for most small-cap companies to expand and maintain a high-margin operation.

This is why investors should pay attention to today’s list. While not immune to the trend, these stocks do have a few tailwinds that can help them maintain a bullish outlook in the coming months.

Why Rising Yields Won't Shake Sprouts Farmers Market Stock

Whether the economy is booming or busting, whether yields are high or low, Sprouts Farmers Market has the benefit of being a consumer staples stock. This stability is reflected through the company’s relatively low beta of 0.56 to offer investors the technical safety they need while markets make up their minds.

Then, there’s the take from Wall Street analysts, particularly those at Goldman Sachs. To start November 2024, these analysts reiterated their “Buy” rating on Sprouts Farmers Market stock, this time boosting their valuations to a high of $157 a share from a previous $127.

To prove these new targets right, the stock would need to rally by as much as 14% from where it has already rallied to post-election. That is one way to ride the small-cap rally without risking the potential ceiling these higher yields are threatening to place.

How a Metal Supercycle Could Drive Mueller Industries Stock Higher

The market’s reaction to the election also suggests a new commodity super cycle, born of the increased business activity that would come globally. This is where Mueller Industries, a copper and aluminum producer, comes into play.

Shares of Tesla Inc. (NASDAQ: TSLA) are up by 12% in a single day to reflect the expected demand for electric vehicles as an election tailwind. Mueller Industries will benefit as copper is an essential material for battery-making. Knowing this, Wall Street analysts have much work to do as new price targets and ratings need to be made.

The stock is already up by 10% to open with bullish post-election sentiment, and the fact that it is now trading at a new 52-week high gives investors a glimpse into the future momentum that could be had in this name.

Why HealthEquity Stock Gains Institutional Support for Post-Election Growth

Over the past 12 months, HealthEquity stock has attracted up to $1 billion in institutional capital, no small achievement for a small-cap stock with a market capitalization of only $8.6 billion.

This bullish sentiment among investors could be credited to the company’s financials, which, as any technology company, sponsor a gross profit margin of up to 64.9%. These high margins allow the company to navigate a rising yield environment with relative ease, and investors need to keep that front and center.

Markets are the bullish for HealthEquity stock compared to its peers, as judged by its willingness to pay a price-to-earnings (P/E) ratio of up to 81.4x compared to the business services’ average valuation of 19.5x P/E. Stocks that are thought to grow at higher rates typically command a premium, and HealthEquity stock is no exception.

24/7 Automated Profits in Crypto

The 4th quarter of 2024 is shaping up to be one of the most explosive periods for crypto in recent memory. But here's the thing: most people won't be able to keep up with the pace of the market.

But there's a way to trade this market with precision – without the stress, without the guesswork.

Macro Headwinds Send Microchip Technology Stock to the Buy Zone

Microchip Technology Incorporated (NASDAQ: MCHP) has the power to withstand its headwinds in 2024 and sustain the uptrend in its share price. The uptrend, begun in 20216, has increased the stock’s value by 300%, including the 2024 price correction, and another 300% upside is coming for those prepared to wait. Not only are the company’s mixed-signal semiconductor products critical to technology, but a rebound in demand is coming in 2025 that will be the beginning of a multi-year upcycle.

2024’s headwinds include a massive inventory correction resulting from COVID-related supply chain issues that will soon pass. OEMs overstocked many components in 2022 and 2023, trying to front-run supply chain issues.

2025’s tailwinds will include normalized demand patterns from OEMs, falling interest rates, and improving demand across consumer end-markets as interest rates fall. End markets range from automotive to mobile, personal computing, the IoT, and every industry that relies on uninterrupted communication between components and devices.

Microchip Technology Sustains Financial Health Despite Headwinds

Microchip Technology's FQ2 2025 revenue is slightly better than expected compared to the consensus reported by MarketBeat, but not good. It is down 48.4% yearly to $1.16 billion, a nearly decade-low. The decline is due to sluggishness in most end markets, with automotive singled out by management as the weakest link. Strengths were seen in the data center business, which is expected to drive growth in 2025 but is insufficient to offset the broader weaknesses.

The margin news is also mixed, coming in better than expected despite a significant decline compared to last year. The critical detail is that the net income of $250 is insufficient to generate positive cash flow for the quarter but sufficient to sustain the company’s financial health until the business rebound begins. That’s a critical detail because the company has maintained solid cash flow growth throughout market cycles and a robust capital return.

The guidance isn’t favorable, with Q3 results expected below the analysts' consensus, but the business bottom may be near. Management noted “green shoots” in prior quarters' reports and said they are advancing, if unevenly, including increased expedited orders, which point to improving end-market demand. With the FOMC on track to cut its base rate to 4% or lower by mid-year 2025 and end-market inventory normalization well underway, the bottom for business may indeed be in. A rebound could begin in early 2025 and gain momentum as the year progresses. Analysts forecast a 20% revenue and 70% earnings rebound in 2025.

Microchip Technology's Strong Balance Sheet Sustains Distribution Growth

Microchip Technology faces headwinds in 2024 but remains strong enough to sustain and grow its capital return, increasing the dividend distribution by 3.6% for Q3. The increase is down from prior years, slowing along with the business, but expected to sustain in 2025, keeping the stock on track for inclusion in the Dividend Aristocrats later this decade.

Due to the stock price correction this year, the dividend yield is at the high end of the historical range, running near 2.5%, but there is a red flag. The payout in 2024 is more than earnings, which raises the question of sustainability. If business does not improve, a dividend cut is likely. Until then, the balance sheet remains in fortress condition with long-term debt less than 1x equity and 0.28x assets.

The Technical Outlook: MCH Stock Returns to Trend

The price action in MCHP stock corrected more than 20% from the 2024 peaks as the pandemic-driven bubble burst. Now, with inventory normalization underway and the stock price corrected from the COVID bubble, the stock price aligns with long-term trends where support is likely strong. The trend line has produced numerous rebounds since 2016, each resulting in new highs for the stock. A move to new highs is worth 40% in upside, not counting the dividend and share repurchases, which also support the stock’s price.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.