Ticker Reports for July 26th

3M Surprises and Rebound Accelerates: It Isn't Too Late To Get In

3M’s (NYSE: MMM) rebound is gaining momentum because of surprisingly good results. Today’s story is that repositioning efforts are taking hold and driving improved profitability while litigation risks dwindle. The takeaways from the Q2 report include better-than-expected top and bottom-line results, organic sequential growth in all segments, improved margin, and increased guidance that affirms the shift in analysts' sentiment. That shift points to higher share prices and the potential for a sustained rally that could last several quarters.

Analysts have yet to revise their estimates and targets based on the Q2 results but will likely increase them because the trend leading into the report is bullish. It includes numerous upgrades and price target revisions that are leading the market higher, lifting the sentiment to Moderate Buy from Hold and the price target by 10% in the last ninety days.

The most recent targets have the stock trading between $110 and $140, which puts consensus near $125 and more than 10% above the post-release price action. Post-release price action is bullish, taking the stock up more than 5% to set a fresh multi-year high. Because the move breaks resistance at a critical level, a complete technical reversal is in play; this stock could trend higher for the next four to six quarters, possibly rising 60% to 70% to reclaim the $170 level.

3M’s New CEO is Already Paying Off for Investors

3M got a new CEO as part of its restructuring efforts, which is already paying off. The company contracted slightly compared to last year, about 0.5%, but primarily due to the spin-off of the medical unit earlier this year. The organic, ongoing business is the significant detail today, growing contrary to expectations. The company reported $6 billion in adjusted revenue, up 1.1% compared to last year, outpacing the consensus estimate by 290 basis points. The strength is due to organic growth in all segments aided by pricing actions to offset inflation.

Another area of strength is margin. The company widened its GAAP and adjusted operating margins due to improved cost structures, internal efficiencies, and the declining impact of litigation costs. The salient details are that GAAP earnings from continuing operations are up 100%, while adjusted EPS from continuing operations is up 39%. Adjusted earnings outpaced the Marketbeat.com consensus estimate by $0.25, and cash flow was robust.

The catalyst for higher share prices was the guidance. The strength in earnings led management to improve its guidance by raising the low end of the EPS target range. 3M now expects full-year earnings to range from $7.00 to $7.30, a range whose midpoint exceeds market expectations. Another increase may come next quarter.

3M Is Back On Track for Distribution Increases

3M recently cut its dividend payout to preserve capital and aid the turnaround but is already back on track for distribution growth. The current payout is $2.80 annually and $.70 quarterly, with a 65% free cash flow payout ratio in Q2, including repurchases, which leaves room for accelerated returns. The dividend is attractive as it is, yielding about 2.75%, with shares in the lower portion of a trading range and reliable. However, the earnings outlook, cash flow, and balance sheet suggest that increases will come soon. Accelerating capital return will be a catalyst for higher share prices.

The balance sheet highlights include a reduction in shareholder equity, but this is due to Solventum's (NYSE: SOLV) spinoff. The offsetting factors are the cash-flow positive quarter, a doubling of cash reserves, and debt reduction. Leverage remains low, below 3X equity, and should improve as the year progresses, improving the outlook for distribution increases.

The repurchases were slowed in 2023 due to pending litigation but are ramping higher. Repurchases failed to offset dilutive actions on a YOY basis but have reduced the count sequentially and are expected to continue.

3M Breaks Resistance: Opens Door for a Sustained Rally

3M’s price action is significant because it broke critical resistance. Critical resistance is near $105 and consistent with lows set in 2020 and a support break in 2022/2023. The takeaway is that this market is now above the baseline of a Head & Shoulders reversal that could quickly add another $30 to the stock price. Critical support is now at $105; a move to retest that level should result in a solid buy signal, but there is risk. A move below $105 could keep this stock range bound for the foreseeable future.

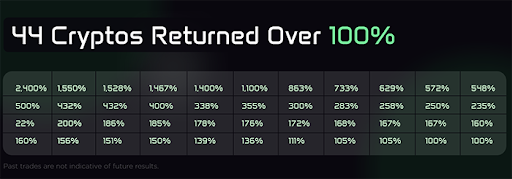

Exposed: 3 CENT Crypto to Explode August 19th?

Chris Rowe – the man who recommended Amazon in 1998… Bitcoin and Ethereum in 2017…

And has spotted 44 different coins that have returned over 100%...

Today, he is now making the biggest crypto call of his ENTIRE career…

Skechers Stock Shows Strength Among Consumer Discretionary Sector

Some names in the retail and apparel sectors have made a splash in investors’ monitors in recent weeks, even months. Unfortunately, the attention is founded on seriously bearish price action, like the fact that shares of Lululemon Athletica Inc. (NASDAQ: LULU) are now trading at only 48% of their 52-week high, which is dangerously close to making a new 52-week low.

Another unlikely name to be trading near a 52-week low is Nike Inc. (NYSE: NKE). Management issued lower-than-expected financial guidance for the rest of the year, sending the stock into a shock selloff. Nike stock is now trading at 58% of its 52-week high, or within 1% of a new 52-week low, to match the bearish price action seen in Lululemon shares.

But, there is one other mention inside the Consumer Discretionary Select Sector SPDR Fund (NYSEARCA: XLY), one that hasn’t been suffering from that much of a bearish price action lately. Shares of Skechers Inc. (NYSE: SKX) trade much closer to their 52-week highs, at 85%, to show investors a different side of the consumer discretionary sector. Here’s why Skechers stock might see an even brighter future ahead.

Financial Momentum Paves the Way for Higher Stock Prices

The company recently announced its second quarter 2024 earnings results, showing the market just why Skechers stock is worth considering. In the press release, management proudly mentioned the company's record sales, up to 7.2% growth to a net $2.16 billion.

However, the benefits don't stop there for shareholders; Skechers' gross margins rose by 220 basis points in the year, reaching a net 54.9% gross margin. The shoe behemoth operates on a much lower 44.6% gross margin compared to Nike's financials.

Retaining this much capital from each sale enables Skechers management to safely and effectively reinvest into other business growth areas. Looking at the past 12 months of returns, Skechers generates up to 11.3% return on invested capital (ROIC) rates, which is probably why the stock outperforms others in the sector.

Annual stock price performances tend to match the ROIC rate over time, and the path is paved for Skechers to continue to create high returns on capital to do this. This confidence is simple: the company has more exposure to international markets. It relies on more than just American demand.

With gold prices hitting a new all-time high, as nations stockpile gold reserves, investors can take this behavior as a vote of no confidence on the U.S. dollar and the economy, so stocks with a higher international sales exposure could become a preference.

This confidence is also quantified for investors, valued at up to $1 billion. That's how much management will allocate toward Skechers' share buyback program, representing over 10% of the company's market capitalization. This is a very aggressive rate, signaling that insiders believe the stock to be cheap today.

And that opinion doesn't stop with management; others on Wall Street would agree.

Wall Street Shows Optimism for Skechers Stock

Overall, Wall Street analysts forecast up to 13.9% EPS growth in the next 12 months for Skechers stock, which aligns with Nike's projections for 13.1% despite Skechers being a fraction of Nike's size.

Leaning on these growth projections, other analysts, such as those at Morgan Stanley, found it easier to value Skechers stock. These analysts set a price target of $80 a share, daring it to rally by 25.6% from its current price.

As another quality stamp check, investors can note that the Vanguard Group (Skechers' biggest shareholder) boosted its stake in the company by 0.8% in the past quarter. While this may not sound like much in percentage terms, that increase would translate into a net $779.5 million investment today.

If that wasn't enough for investors to consider another look into Skechers stock, then decrypting the market's message might do it. Outlying valuations can sometimes be the market's way of saying that it likes – or dislikes – a stock, depending on where that valuation multiple is.

On a price-to-earnings basis (P/E), Skechers' 16.8x multiple will command a premium of nearly 100% compared to the footwear industry's average 8.9x P/E.

There's typically a good reason why markets are willing to bid a stock up in its valuation multiples and why this stock will, in turn, trade near its 52-week highs. Seeing all of the evidence on a fundamental and technical level, investors could consider adding Skechers to their watchlists.

Tim Sykes' Urgent Trade Alert: "Make this move now"

WARNING: 80 Wall Street banks are gearing up for MASSIVE D.C. shock (June 12)

This $2 trillion D.C. shock is NOT about Trump or Biden dropping out of the race…

Tech Stocks Tumble, These Stocks Present Buying Opportunity

As earnings season unfolds and several mega-cap tech stocks, including members of the "Magnificent Seven," have reported, the overall market and tech sector have seen significant declines in recent weeks. The XLK technology sector ETF has dropped nearly 6% this month and is now down over 10% from its recent 52-week highs. Similarly, the broader market, represented by the SPY ETF, is down nearly 5% from its 52-week high and over 2.5% this week.

Several well-known tech stocks have experienced sharp declines in this environment, making headlines. Specifically, CrowdStrike (NASDAQ: CRWD), Advanced Micro Devices (NASDAQ: AMD), and HubSpot (NASDAQ: HUBS) have all seen their share prices drop close to or over 30% from their 52-week highs. Given this rapid selloff, is it time to consider buying shares of these companies on the dip?

Advanced Micro Devices

AMD's stock has sharply declined, falling nearly 40% from its 52-week high and down over 6% year-to-date. This decline comes amidst concerns that the Biden administration may impose stricter regulations on products imported from overseas that use American technology. While such export controls could impact sales in the short term, they are unlikely to dampen the growing demand for advanced chips, particularly those used in data centers and artificial intelligence (AI) model training—a lucrative market for AMD.

Over the past year, analysts have significantly raised their earnings forecasts for AMD, highlighting the company's strong growth prospects. AMD's data center revenue is a crucial driver, having surged 80% year-over-year in the latest quarter. Advanced Micro Devices (AMD) is set to release its next quarterly earnings report on Tuesday, July 30th, 2024. The consensus forecast for this quarter's earnings per share (EPS) is $0.47, up from $0.40 reported for the same quarter last year. Currently, the stock has a Moderate Buy rating based on twenty-nine ratings, with a consensus price target of $194.97, forecasting a whopping 41% upside.

HubSpot, Inc.

HubSpot, a $25 billion company, provides a cloud-based customer relationship management (CRM) platform for businesses across the Americas, Europe, and the Asia Pacific. The stock fell sharply after Google parent Alphabet walked away from acquisition talks, causing HUBS to drop 28% from its 52-week high and nearly 15% for the month.

Despite the setback, this dip could present a buying opportunity for a company with a strong track record of steady revenue growth and a growing global customer base of over 215,000 small to medium-sized businesses. While enterprise software spending faces challenges due to economic uncertainties, HubSpot's revenue grew 23% year over year last quarter, showcasing its resilience. The company reported earnings on May 8th, 2024, posting $0.01 EPS, significantly beating the consensus estimate of ($0.26) by $0.27, with revenue of $617.41 million, exceeding expectations of $597.12 million. HubSpot is scheduled to release its following earnings report on August 7th.

CrowdStrike Holdings

CrowdStrike Holdings, a $61 billion cybersecurity giant specializing in cloud-native endpoint protection, has recently faced a significant drop in its stock price. The company has seen its value plummet over 35% from its 52-week high and 34% this month alone. This sharp decline is primarily due to a faulty update to its Falcon platform, causing a global IT outage that affected a wide range of critical sectors, including banks, airports, hospitals, retailers, businesses, and government agencies. The incident has led to considerable disruption and raised questions about CrowdStrike's reliability and prospects.

Despite the recent setback, CrowdStrike's core business remains strong, with projected earnings growth of 55% for the year. In its latest earnings report on June 4th, 2024, CrowdStrike reported an EPS of $0.20, just shy of the $0.21 consensus, with revenue of $921.04 million surpassing expectations. The company has shown impressive annual sales growth of 66.22% over the past five years, with a 33% increase in quarterly sales compared to the previous quarter. However, the fallout from the Falcon update incident has created uncertainty, making CrowdStrike a potentially volatile investment. Despite recent challenges, this dip-buy opportunity may appeal to those with a higher risk appetite who are confident in the company's long-term prospects.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.