Dear Reader,

When ChatGPT launched, it sparked a revolution.

In just two months, it grew to 100 million users.

And now…

800 MILLION people use ChatGPT every week.

But until now…

OpenAI is reserved only for the rich elites.

Billionaires like Peter Theil, Elon Musk, and Reid Hoffman… they all got in early.

But you were locked out.

That changes today…

|

Pre IPO Claim in ChatGPT (SEE THE FREE TICKER HERE)

As OpenAI gears up for the largest IPO in history… over $1 trillion…

I’m going to show you the secret way to get exposure early… BEFORE the IPO.

Keep in mind, OpenAI’s trillion dollar IPO is going to be bigger than Apple… Microsoft… even Amazon.

And people turned $10,000 into tens of millions since the 80’s and 90’s thanks to those stocks going public.

In fact, Apple turned 300 people into millionaires just on the first day!

Getting in early is a huge opportunity… but you need to act quickly.

The IPO announcement could come as early as March 18.

Get in Early on OpenAI’s Trillion IPO Here

Yours in smart speculation,

Karim Rahemtulla, Co-Founder

Monument Traders Alliance

Freeport-McMoRan's Rally Is Over—But the Bull Case Isn't

By Chris Markoch. Publication Date: 3/6/2026.

Key Points

- Freeport-McMoRan’s Grasberg restructuring secures operations through 2041 but reduces its economic ownership, creating both stability and lower earnings leverage.

- Rising copper demand from EVs, data centers, and electrification supports the long-term bull case for FCX stock.

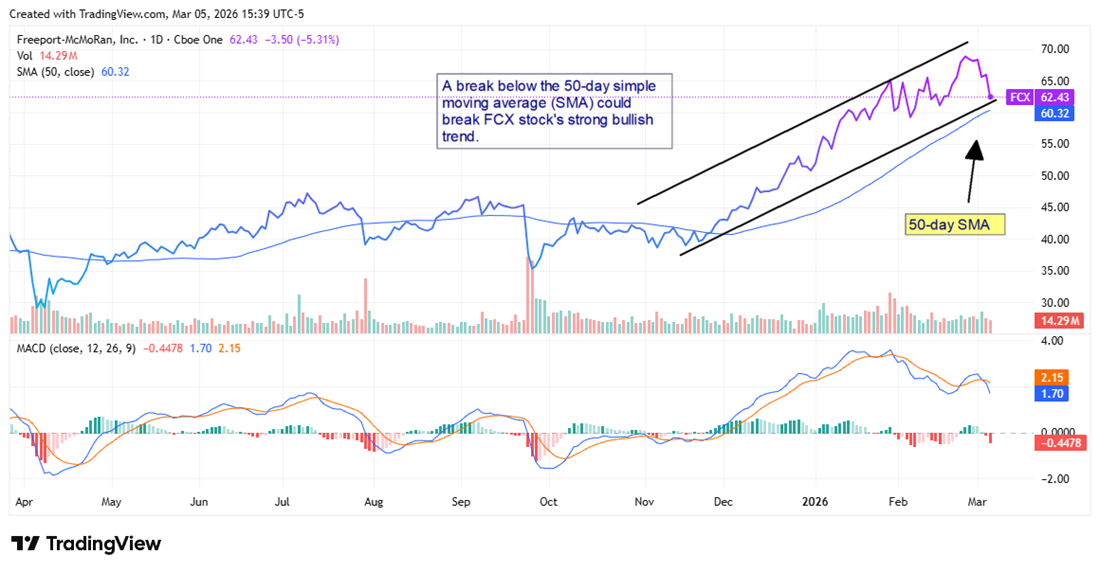

- After an 80% rally in four months, technical indicators suggest FCX stock may pull back toward the $55–$57 range before its next move higher.

- Special Report: Elon Musk's $1 Quadrillion AI IPO

Freeport-McMoRan Inc. (NYSE: FCX) entered 2026 riding a wave of bullish sentiment. The company is one of the world's largest copper miners at a time when basic materials stocks — and mining stocks in particular — are viewed as relatively safe investments.

After surging nearly 20% following its Jan. 22 earnings report, FCX has given back almost all of those gains. It recently closed near $62, hovering near its 50-day moving average around $60.

A personal warning from Martin Weiss (Please read) (Ad)

The Fed is counting on the fact that ordinary Americans won't read a 93-page document until it's too late. I've read it and that's why I'm begging you to act while you still can.

Get the 4 "Fed-proof" steps right now.For investors who missed the November 2025 rally, this sell-off may seem puzzling.

Dig a little deeper and a more nuanced picture emerges: the long-term bull case remains largely intact, which argues for a buy-the-dip opportunity. Still, near-term valuation concerns and geopolitical complexities could push the stock lower before it rebounds.

The Grasberg Factor: A Calculated Bet on Indonesia

The Grasberg mine in Papua, Indonesia, is one of the world's largest copper mines and one of its largest gold mines. It's also central to the bull case for Freeport-McMoRan.

On Feb. 18, Freeport announced that it had restructured its relationship with the Indonesian government. Specifically, the company traded a majority stake in the Grasberg operation to state-owned PT Indonesia Asahan Aluminium (Inalum) in exchange for operational continuity and a long-term contract of work.

The arrangement locked in Freeport's right to operate through at least 2041, providing a runway that matters given where copper demand is headed.

This was pragmatic dealmaking under pressure; shareholders pushed FCX to an all-time high within a week of the announcement.

However, as the stock has fallen, investors appear to be weighing the trade-off: Freeport now holds a minority economic interest in the mine instead of a majority one, meaning lower per-share earnings leverage to Grasberg's output than before.

Nonetheless, Grasberg's ore body is enormous and its gold and copper grades are rich; even a minority stake generates meaningful cash flow. This isn't a diminishing asset, and that cash flow should become more valuable as electrification increases demand for copper.

The Copper Demand Thesis Is Not Going Away

The long-term bull case for FCX ultimately rests on copper, and that story has never been stronger. In 2022, investors were focused on electric vehicles (EVs) and renewable energy infrastructure. In 2026, the narrative now also includes grid-scale battery storage and data centers.

Demand for copper is surging while supply is not keeping pace. There are three key reasons for that.

- New large copper deposits are increasingly rare.

- Many are located in geopolitically difficult regions.

- The ones that are accessible require years and billions of dollars to bring online.

Freeport, with world-class assets in Arizona, Peru, and Indonesia, is one of a small number of companies capable of meeting that demand at scale.

Analysts broadly agree that the structural deficit expected to emerge in the late 2020s hasn't been priced out. Macroeconomic concerns — slower Chinese growth and the effects of higher interest rates on industrial demand — create short-term noise, but the electrification tailwind is generational.

Gold Adds a Second Engine

Adding to the bull case for FCX is the company's exposure to gold. Grasberg is not a copper mine that produces a little gold on the side; it is a genuine dual-commodity powerhouse.

That matters now: gold is in a multi-year bull cycle driven by central bank buying, de-dollarization trends, geopolitical uncertainty, and investor demand for hard assets. As gold prices remain elevated, Grasberg's gold output contributes increasingly to Freeport's earnings.

This gold exposure acts as a partial hedge against copper price volatility and provides FCX with a revenue stream that is less dependent on industrial demand. For long-term investors, that dual-commodity structure is a genuine differentiator among the major mining stocks.

The Chart Is Sending a Warning Signal

The technical picture tells a cautionary tale for short-term positioning. FCX rallied strongly from roughly $38 in October 2025 to a peak just above $70 in early February 2026. A move of more than 80% in roughly four months almost always requires consolidation.

The moving average convergence/divergence (MACD) has crossed bearish, with the signal line pulling away from a declining MACD line. Combined with the stock breaking below its recent trading range, momentum favors more downside—or at best a sideways grind—before the next leg higher.

The 50-day moving average at $60.32 represents the first meaningful support level. A sustained break below that would open the door to a test of the $55 area, which was a prior consolidation zone on the way up.

Meta and Rocket Lab Insiders Sell Shares—So Why Is Wall Street Buying?

By Jeffrey Neal Johnson. Publication Date: 3/3/2026.

Key Points

- Institutional investors continue to pour capital into Meta Platforms and Rocket Lab despite high-profile insider selling by executives.

- Meta Platforms continues to demonstrate operational efficiency with strong revenue growth and healthy profit margins that attract smart money.

- Rocket Lab maintains a massive backlog of government contracts, which provides long-term revenue visibility and stability for shareholders.

- Special Report: Elon Musk's $1 Quadrillion AI IPO

It is a confusing time for retail investors. Markets are trading near record highs, companies are posting massive revenue numbers, and excitement around technology and space exploration is palpable. Yet a troubling trend has emerged in the headlines: the very people running these successful companies—CEOs, CFOs, and COOs—are selling stock at an aggressive pace.

When executives liquidate millions of dollars in shares, it often triggers alarm bells. Investors naturally worry that insiders know something the public does not. Is the top in? Are growth prospects slowing? Seeing a chief financial officer (CFO) dump stock can feel like watching the captain put on a life vest while assuring passengers the ship is unsinkable.

A personal warning from Martin Weiss (Please read) (Ad)

The Fed is counting on the fact that ordinary Americans won't read a 93-page document until it's too late. I've read it and that's why I'm begging you to act while you still can.

Get the 4 "Fed-proof" steps right now.However, panic is rarely a profitable strategy. While insider selling creates fear, a closer look at the data can reveal a powerful counter-signal: institutional accumulation. Hedge funds, pension funds, and investment banks often buy the same shares executives are selling. This divergence between individual profit-taking and institutional conviction can present opportunities for investors who know where to look.

Zuckerberg's Team Cashes Out, But Wall Street Buys In

Meta Platforms (NASDAQ: META) has been a dominant force in the market, with its stock trading around $655 as of early March 2026.

That rally reflects integration of artificial intelligence and robust advertising revenue.

Recent filings show Meta's executives taking substantial chips off the table. In Feb. 2026 alone, CFO Susan Li sold roughly $35 million worth of stock. COO Javier Olivan also executed multiple sell orders throughout the month.

In total, eight insiders have sold over the last 12 months, with no insider buys recorded. From an outsider's perspective, seeing top executives reduce their holdings can look like a lack of confidence.

Understanding Rule 10b5-1 Trading Plans

It is crucial to understand the mechanism behind many of these trades. Most were executed under Rule 10b5-1 trading plans—pre-scheduled plans that automatically sell stock at set times or prices, often established months in advance.

- Legal protection: These plans shield executives from insider trading allegations. They cannot simply decide to sell because of newly learned material information; the sale dates were likely set earlier.

- Diversification: Executives are often paid in stock. Selling is the only way to convert that paper wealth into cash for taxes, real estate, or portfolio diversification.

- Rational planning: With the stock near all-time highs, locking in gains is standard financial planning and does not necessarily indicate a bearish view of the company's future.

Fundamentals Override Insider Fears

While insiders sell, the smart money is buying. Data from the last 12 months shows a net institutional inflow of over $100 billion into Meta stock. Recently, billionaire investor Bill Ackman reportedly acquired a multi-billion-dollar stake, arguing the company remains attractively valued despite its rally.

Institutions are focusing on fundamentals rather than the optics of insider trades.

- Earnings beat: In late Jan. 2026, Meta reported earnings per share (EPS) of $8.88, comfortably above estimates of $8.16.

- Revenue growth: Revenue climbed 23.8% year-over-year, showing acceleration in the company's core advertising business.

- Margins: Despite heavy AI infrastructure spending, Meta maintained net margins above 30%, signaling operational efficiency.

- Valuation: With a price-to-earnings ratio (P/E) of roughly 27.9, Meta is trading at a reasonable multiple for a company growing revenue at over 20%.

For Meta's institutional investors, the thesis is simple: Meta is a cash-flow machine with a dominant market position. They see the current price not as a peak but as a stepping stone toward higher valuations.

Blast Off: Why Institutions Are Chasing a Space Stock

The divergence between insider selling and institutional buying is even more pronounced at Rocket Lab USA (NASDAQ: RKLB). The aerospace company has seen its stock surge from the mid-teens to over $70 in about a year. That explosive growth has led to massive liquidity events for the leadership team.

The numbers are striking. In Dec. 2025, CEO Peter Beck sold more than $140 million in stock. CFO Adam Spice followed with sales exceeding $100 million in Jan. 2026. Those are large figures that can spook retail investors.

Context matters. Rocket Lab's leadership spent years building the company from a startup to an industry player with a roughly $37 billion market cap. For founders and early executives, selling shares after a 400% run-up is a life-changing event.

Those sales often reflect realizing past success rather than a lack of faith in the company's future. If the leaders believed the business was doomed, they likely would have sold earlier at much lower prices.

Why Wall Street Loves Rocket Lab

Wall Street clearly does not view these sales as a red flag. Institutional ownership in Rocket Lab has surged to nearly 72%. Over the last 12 months, institutions purchased $4.96 billion in shares while selling only $1.51 billion. Major funds like Vanguard and Baillie Gifford are absorbing supply created by insiders.

Why are they buying? Institutions look forward, not backward. They are focused on three primary catalysts:

- Massive backlog: Rocket Lab sits on a $1.85 billion backlog. Contracted work gives revenue visibility for years, much of it backed by government contracts from the Space Development Agency (SDA).

- Record revenue: The company closed 2025 with record revenue of $602 million, validating its business model.

- Strategic position: Rocket Lab has effectively cornered the small-to-medium launch market outside of SpaceX.

Even the recent delay of the Neutron rocket to Q4 2026 has not significantly deterred accumulation. The delay, attributed to a manufacturing defect in a tank test, is being treated by analysts as a temporary setback. The sizable SDA contracts and Rocket Lab's satellite production capabilities keep the long-term growth thesis intact.

The Bigger Picture: Wealth Transfer

When analyzing stocks like Meta Platforms and Rocket Lab, it is easy to get swept up in headlines. Insider selling makes for dramatic news, but it rarely tells the full story. Executives sell for personal reasons; institutions buy for profit.

The divergence we are seeing today is a classic wealth transfer: insiders are cashing out on the growth of the past decade, while institutions position themselves for the growth of the next decade.

For investors, the actionable takeaway is clear:

- Meta Platforms: The AI fatigue narrative appears to be noise. Strong institutional support suggests the stock remains a core holding for long-term portfolios.

- Rocket Lab: The size of the backlog and the company's dominant position in the space economy outweigh the optics of insider selling. Institutional accumulation suggests the Neutron delay is a buying opportunity for investors willing to accept higher volatility.

Ultimately, while insiders may be taking profits, the market's biggest players are betting heavily that these rallies are far from over. Following the flow of institutional capital often provides a clearer signal of value than the tax planning or diversification moves of a handful of executives.

Investors seeking long-term growth may want to add Meta Platforms to their watchlist on any dips caused by insider-selling headlines, while aggressive growth investors might view Rocket Lab's current pullback as an entry point, given the strong institutional support and its $1.85 billion backlog.

This email content is a sponsored message provided by The Oxford Club, a third-party advertiser of Earnings360 and MarketBeat.

This ad is sent on behalf of Monument Traders Alliance. 14 West Mount Vernon Place Baltimore, MD 21201. If you would like to optout from receiving offers from Monument Traders Alliance, please click here.

If you have questions or concerns about your subscription, feel free to contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from Earnings360, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 North Reid Place, Suite 620, Sioux Falls, SD 57103-7078. United States of America..