Snowflake's business acceleration has just begun and will take the company and its stock higher over time, according to analysts who are... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Thomas Hughes

Snowflake’s (NYSE: SNOW) Q2 results highlight the global shift to AI. Now that the infrastructure build is well underway, sectors, industries, and businesses are embracing the application of AI, which requires data services that Snowflake is happy to provide. Its data lake-based services span the data lifecycle, enabling the storage, management, analysis, and sharing of data across cloud environments. Cross-cloud operability is critical to Snowflake’s appeal and utility for AI, making it a go-to source for many large businesses and a crucial component of global AI infrastructure. Snowflake’s Accelerating Business Leads to Beat-and-Raise Quarter Snowflake had a robust quarter, accelerating its growth compared to the same period last year and the prior quarter. The $1.14 billion net revenue is up 31.2% year over year, outpacing consensus estimates by more than 400 basis points due to strength in client counts and penetration. Product revenue grew by 32%, a significant increase given that it accounts for nearly 100% of the revenue. Large clients' revenue was up by 30% and the net retention rate was 125%. RPO, a key business indicator, was also solid and up by 33%. The margin news is also strong. Although there was some contraction in gross margin and GAAP results, the losses are primarily non-cash in nature. The adjusted results are more robust, including $0.35 in EPS, outperformance, and positive free cash flow. The adjusted EPS is nearly double compared to the prior year, more than 3000 basis points ahead of consensus, with earnings expected to remain strong through the year’s end.

Snowflake’s Guidance Will Sustain the Bullish Trend in Analyst Sentiment Snowflake’s guidance is another area of strength and one that is sustaining the uptrend in analysts' sentiment. The company raised its targets for revenue and earnings more than anticipated, catalyzing numerous price target increases. The revisions put the market in the high-end range, which tops out at $285, a nearly 20% upside from critical resistance levels, and higher highs are likely. Other trends revealed by MarketBeat data include increased coverage and a firming sentiment, with the number of Sell and Holds declining and Buys and Strong Buys increasing. As of late August, this stock is rated a Moderate Buy. Insider selling poses a risk to investors, but it is small and offset by robust institutional activity. While several insiders have been selling in 2025, the total number of shares sold is small, and insider holdings remain substantial, accounting for over 6% of the stock. The bulk of sales is led by former CEO Frank Slootman, who is well-known for taking the business public. His sales are part of a previously disclosed plan and are being absorbed by the institutional community. Institutional activity has underpinned Snowflake’s stock price action all year. The group was bullish in 2024 but ramped up the buying in 2025, netting more than $2 in shares for every $1 sold. They provide solid support for this market, owning more than 65% of the shares, as reflected in the stock price action, which has been trending sideways within an extensive range for the last few years. Snowflake Poised for New Highs in 2025 Following the release, Snowflakes' price action was very bullish, rising by more than 12% to show support in the low $190 range. This level aligns with the 30- and 150-day EMAs and is a strong support level unlikely to be broken soon. The likely scenario is that Snowflakes' price action will continue to move higher and retest the top of the range by the end of calendar Q3 2025. A move to new highs is likely because of the results, guidance, and analyst trends. The late-August consensus of $240 is sufficient to set a three-year high, and it is expected to continue trending higher as the quarter progresses.

Read This Story Online Read This Story Online |  Imagine a bull market so powerful, every single investor became a millionaire. Not by finding the next NVIDIA or Bitcoin, but by owning a simple index fund.

It sounds impossible. Yet it happened – just a short time ago. Now a legendary figure says: "Brace yourselves. It's about to happen here, in America. But fair warning – it could be the worst thing that ever happens to you."

This story has received little coverage in the press. But if history repeats, it could bump tens of millions of Americans into a 7-figure net worth practically overnight. Click here for the full story. |

| Written by Chris Markoch

Concerns about inflation still dominate this market. In April and May, the immediate concern was that the Trump administration's tariff policy would cause a sharp spike in inflation. That hasn’t been the case, although some companies, particularly retailers, continue to report tariff headwinds. However, the current concerns about inflation center around interest rates. The CME FedWatch tool puts the chance of a 25-basis point rate cut in September at around 87%. However, lower interest rates have a stimulative effect on the economy. That means that inflation will almost certainly increase, including for commodities like oil that have been in check so far in 2025. That’s good news for a blue-chip stock like Chevron Corp. (NYSE: CVX). Here’s another reason. Dividend growth stocks are one of the only investments that give investors an opportunity to keep up with inflation. Chevron has increased its dividend for 38 consecutive years, putting it in the exclusive category known as dividend aristocrats. However, the company also has a strong track record of delivering share buybacks to shareholders. In the company’s second quarter, Chevron delivered $5.5 billion to shareholders between dividends and buybacks. Not a Contrarian Play Energy stocks, particularly oil stocks, have been under pressure for much of the year. The problem with oil has been that companies like Chevron have increased their output for the last 12 months, and the market is well supplied. Plus, investors are concerned that alternative energy still represents an existential threat to oil and gas companies. Lower interest rates may not immediately spark demand. However, if manufacturing and industrial output increase, that will be bullish for crude. Plus, if consumers get relief in time for the holiday season, it could spark a slight revival in transports, which would also be bullish for oil. The alternative energy threat is really a win-win situation for Chevron. First, it will be years and more likely decades before the world has enough renewable energy sources to make oil less relevant. Until then, Chevron and other oil companies remain essential for economic growth. At the same time, Chevron hasn’t been ignoring the alternative energy market. The company continues to spend billions on low-carbon initiatives, including: - Renewable fuels – Chevron is one of the largest producers of renewable diesel and sustainable aviation fuel in the U.S. It has joint ventures, including with Bunge, to expand feedstock processing and distribution.

- Carbon capture and storage (CCS) – The company is developing CCS projects in California and the U.S. Gulf Coast, with the goal of storing millions of metric tons of CO₂ per year.

- Hydrogen – Chevron is building out hydrogen fueling infrastructure in California and exploring opportunities in heavy-duty transport.

- Renewable natural gas (RNG) – Through partnerships with agricultural operators, Chevron is converting methane from dairy farms into renewable gas for transportation.

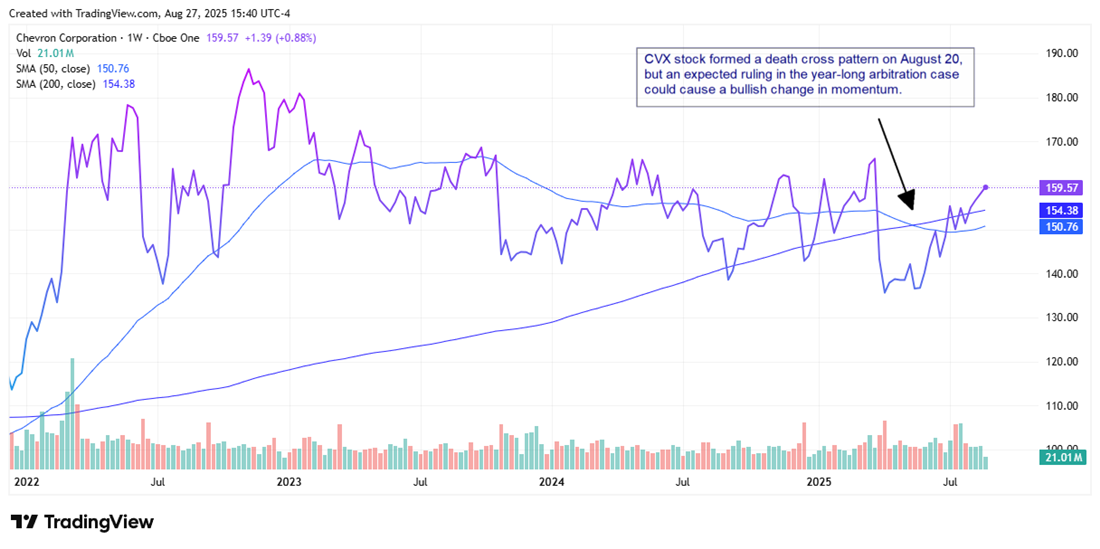

Analysts Forecast a Big Move in CVX Stock Chevron stock is up about 10% in 2025. That approximates its three-year average total return of around 8.8%. It also points to the range-bound conditions that have been in place for Chevron during that time. It’s also a little deceptive because of the spike in CVX stock since early April. Chevron stock formed a death cross on August 20. However, the stock is stabilizing, and the pattern could be reversed quickly. The bullish sentiment is shared by UBS Group. The analyst firm reiterated its Overweight rating on CVX stock and raised its price target to $197 from $186. That’s an approximate gain of 20% from its consensus price target of $163.95.

The company won’t report earnings until early November. However, it could get a catalyst in the waning days of August. That’s when Chevron expects to receive the final ruling regarding the arbitration over Exxon Mobil’s claims to preemptive rights in the Staebroek block in Guyana. This arbitration was sparked after Chevron announced its merger with Hess, which was finalized in July. Read This Story Online |  |

| Written by Chris Markoch

Best Buy Co. Inc. (NYSE: BBY) stock is down 4.6% after the company reported its second-quarter earnings on August 28. The company beat on the top and bottom line and maintained its prior full-year guidance. However, investors appear to be looking beyond the current print and wondering about future growth. For its part, Best Buy hopes the growth will come from its newly launched Best Buy Marketplace. This is part of the company’s evolving digital expansion strategy, which includes improving customers’ online shopping experience while leveraging the retailer’s brick-and-mortar footprint. However, as of the company’s report, the Best Buy Marketplace was only one week old. That means investors won’t have any numbers until next quarter. Even then, they should lower expectations. Best Buy sees this as a multi-year growth initiative that may take years before it delivers a material financial impact. Bullish investors believe the marketplace could revitalize Best Buy’s position in the competitive e-commerce space. However, skeptics note that this idea has execution risks that may outweigh the potential benefits. Could Best Buy Marketplace Be an Amazon-Lite? There are some upsides to a marketplace model that are more than theoretical and could create a network effect. First, Best Buy will immediately expand its product assortment without having the inventory expense. Management reported encouraging initial seller interest that could lead to an acceleration over time. Second, the Best Buy Marketplace could meaningfully increase the company’s bottom line. That’s because the fee-based revenue from third-party sales will be more profitable than the company’s traditional margins. Third, the marketplace leverages Best Buy’s brick-and-mortar footprint. Shoppers can pick up Best Buy Marketplace items in-store or access Geek Squad support, creating an experience that pure online competitors struggle to match. Best Buy Will Need to Stay on Target Analysts lean bullish on BBY stock, but investors should wait to see what the commentary is after the earnings report. Best Buy isn’t the first company to launch a marketplace initiative. However, other retailers have faced challenges with marketplace strategies. Target Plus grew cautiously because scaling third-party sellers while maintaining quality proved difficult. Macy’s marketplace pilot struggled with low seller adoption and brand alignment. Even a success story like Walmart faced slow adoption as sellers struggled with technical integration and traffic. These examples highlight the risks of slow revenue growth and potential brand impact, especially in the early years of a marketplace. Another consideration is cannibalization. Third-party sellers might undercut Best Buy’s own pricing, which could pressure margins instead of boosting them. Finally, some market observers may view the marketplace as a strategic distraction, particularly in light of Best Buy’s earnings report, in which it lowered its forward guidance, which could explain the post-earnings dip in BBY stock. Is a Beat and Stick Report Causing BBY Stock to Slide? The good news was that Best Buy beat expectations on the top and bottom lines. Revenue of $9.44 billion was higher than estimates of $9.28 billion, buoyed by sales of the new Nintendo Switch 2. However, with revenue being up 1.6% year-over-year (YOY), investors could be concerned that YOY revenue would have been negative without the one-time impact of the Switch 2 launch. Best Buy also reported $1.28 in earnings per share (EPS), beating estimates for $1.22. That number, however, was 4% lower than the $1.34 the company posted in the prior year. What may have been more disappointing was that, unlike many other retail stocks, Best Buy maintained its prior full-year guidance. On the earnings call, the company cited, “the uncertainty of potential tariff impacts in the back half, both on consumers overall as well as our business.” Read This Story Online |  On September 15th, the IRS collects another round of quarterly tax payments—targeting self-employed professionals, retirees, and high-net-worth savers.

But the wealthy aren't just writing checks. They're moving fast to protect capital and purchasing power using legal, IRS-compliant strategies.

American Alternative Assets just released the Mar-A-Lago Accord, a free guide revealing how to reduce Q3 tax exposure and reposition wealth before it's drained. Click here to download the guide and protect your assets before Sept 15th. |

| More Stories |

| |

|

|