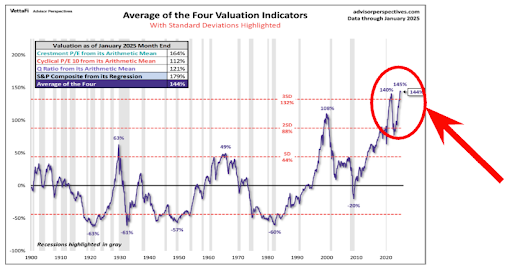

Why are more traders opting for high-risk 0DTE options? The only answer is cost! Right now, stocks are the most expensive they've ever been in history.

Of course this translates to higher prices options – forcing regular traders to fall back to the cheaper, riskier alternative. Here's where the problem is... It's impossible to thrive while trading 0DTE options without having momentum on your side. NO – your regular "momentum" indicator won't cut it. You need REAL-TIME feedback with zero lag and near 100% precision. That's where my top trading engine – Alpha Zone Pro – comes in.

Not only does it report live data of the true market momentum… Giving you room to take positions BEFORE the charts catch up… It also displays the exact point it sees a buy or a sell happening. Giving you a shot at more accurate entries at less than 10% of what regular options cost! Thanks to Alpha Zone Pro… Some of our best students have been able to pile in anywhere from 27% to 77% gains in less than an hour – sometimes multiple times throughout the day. And although we can't make guarantees when it comes to the market… But you're one step away from tagging along. All you have to do is head over here now and get started.

By clicking the link above you agree to periodic updates from The TradingPub and its partners (privacy policy) Roger Scott

Today's Bonus Article Goldman, Morgan Stanley, & BofA: Diverging Paths After EarningsWritten by Sam Quirke

Wall Street just wrapped up a big week for earnings in the financial sector, and if there's one clear thing, it's that not all banks are built the same right now. With rising interest rates no longer the tailwind they once were, and margin pressure becoming a theme, investors are quickly drawing lines between the winners and the also-rans. While all three major bank stocks profiled below have rallied strongly since April, their post-earnings setups diverge rapidly. Let's see which ones are worth chasing and which might be best avoided. Goldman's Rally Might Be Running Out of Steam Of the three, Goldman Sachs Group Inc (NYSE: GS) is the best performer since April, up more than 60% and now consolidating just below all-time highs. On paper, there's a lot to like. The company has just delivered a solid set of Q2 earnings, beating analyst expectations and showing revenue growth of 15% year-over-year. Valuation-wise, it's also solid with a P/E ratio of around 15, not too hot and not too cold. But there's a sense that much of the good news is already priced in. Despite the headline beat, the stock's reaction was muted. Several analysts called it a Hold in the aftermath of Wednesday's report, with Market Perform and Equal Weight ratings dominating the commentary. While shares are still below many of the refreshed price targets, the lack of urgency suggests the near-term upside might be limited unless Goldman can show another gear. There's no question this has been the hottest bank stock of the past few months, but it's also starting to feel like a lot of the easy gains have already been made. Morgan Stanley Has the Momentum Shares of Morgan Stanley (NYSE: MS) haven't rallied quite as much as Goldman's, but its post-earnings setup looks more interesting. Interestingly, though, shares did drop sharply after Wednesday's earnings release, falling as much as 4% before recovering and finishing Thursday in the green. However, the fact that the dip was so quickly bought up points to a strong undercurrent of demand for the stock right now. Heading into the year's second half, there's a lot to like about Morgan Stanley. Fundamentally, the company exceeded earnings expectations this week, with revenue up nearly 12% year-over-year. Management has also been stepping up with shareholder-friendly moves, including a dividend increase and a larger buyback program. The analyst reaction has also been more encouraging than Goldman's, with Keefe Bruyette & Woods upgrading the stock to Outperform earlier this month. The stock's chart is solid, the fundamentals are improving, and the Street is starting to warm up. If you're looking for the name with the most near-term upside potential, this is probably it. Bank of America Still Has Work to Do Bank of America Corp. (NYSE: BAC) has also had a decent run over the past few months, rallying more than 40% since April. However, unlike its peers, it's still trading below its 2022 all-time high, which says a lot. Furthermore, the bank missed revenue expectations in its Q2 report this week, likely weighing on sentiment for the foreseeable future. Investors have had reason to be skeptical, and for now, at least, their skepticism appears justified. While the broader financial sector has been enjoying a bright spell, Bank of America continues to lag its peers on both technicals and fundamentals. There's no real breakout narrative here, and the market seems to know it. To its credit, Bank of America is the cheapest of the three, trading at a P/E ratio of about 13. If you're a deep-value investor willing to stomach more risk, a long-term case must be made. However, in the near term, there are simply better options.

|