Bridgewater Associates, the investment management company founded by Ray Dalio 50 years ago, just invested millions in these three stocks.. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Leo Miller

Bridgewater Associates, founded by famed investor Ray Dalio, loaded up on shares of some big-name stocks in Q4. Bridgewater Associates recently released its Form 13F. Institutional investment managers with more than $100 million in discretionary control over 13F Securities must file this document. It provides transparency into what they own. Stocks and ETFs are two of the biggest 13F security categories. Although Dalio isn’t running the day-to-day investment operations of Bridgewater at this point, he is still involved with the firm. He sits on its Board of Directors and mentors the company’s Chief Investment Officers. His ongoing presence shows that his principles and guidance still shape Bridgewater's investment philosophy and choices. Robinhood: Bridgewater Betting on the Future of This Investment Platform In Q4, Bridgewater massively increased its stake in Robinhood Markets (NASDAQ: HOOD), acquiring an additional 2.1 million shares. Shares of Robinhood have gone on an incredible run over the past several months. Bridgewater has likely achieved impressive returns with this investment. Since Sept. 30, Robinhood’s share price has risen by nearly 153% as of the Feb. 19 close. Excitement surrounding the company’s ability to benefit from increased interest in cryptocurrencies has been an important driver. President Trump’s notable affinity toward crypto adds to this thesis. Indeed, interest in crypto translated to success for Robinhood last quarter. Crypto trading volume, on which Robinhood earns a spread, spiked by 455%. This was one factor that helped the firm to over double its average revenue per user from a year ago to $164. Now, the company has nearly $200 billion in assets under custody and has managed to increase its revenues by more than ten times in just 5 years. It has demonstrated a strong ability to cater to Gen Z and millennial investors. Its one-stop-shop platform, where investors can find both traditional and newer types of assets, resonates with these clients. Trillions in wealth are set to transfer to millennials and Gen Z over the next 20 years. This would be a big tailwind for Robinhood if it could keep these clients happy. PayPal: Bridgewater Increases Stake in Online Payment Giant In Q4, Bridgewater added over 1.1 million shares of PayPal (NASDAQ: PYPL), nearly doubling its position in this name. PayPal shares haven’t had much success since the beginning of Q3, with a return of 0% as of the Feb. 19 close. This is largely due to PayPal’s recent financial results that showed some onlookers underlying weakness in the company. Shares dropped by 13% after the release. As the company is looking to grow profitably rather than at the expense of profit, markets are down on this name. It's possible Bridgewater investors are bullish on this strategy despite the fact that it does risk PayPal losing market share. However, Bridgewater also has notable positions in other companies in the payments industry, like Visa (NYSE: V) and Global Payments (NYSE: GPN). This signals that they may be bullish on the payments space in general. With economic growth and payment digitization both being trends that will continue over time, it makes sense to like this space. Additionally, Visa, Global Payments and PayPal are strong players in different niches within payments. Visa is the leader in card networks, while PayPal dominates digital wallets and online consumer payments. Global Payments ranks fourth in the United States market share in the merchant acquiring space. AT&T: Bridgewater May Have Picked a Side in the Big 3 Telecom Battle Bridgewater’s position in the Big Three telecom company AT&T (NYSE: T) ballooned in Q4 2024. It added nearly 5.2 million shares. Notably, Bridgewater does not have Verizon Communications (NYSE: VZ) and T-Mobile US (NASDAQ: TMUS) in its top 50 holdings. Bridgewater is possibly betting on the positioning of AT&T compared to its two rivals, especially as it pertains to broadband internet. Broadband strategy is one of the biggest differences between these firms. AT&T has the strongest commitment to fiber optics. This technology requires expensive upfront investment, but it has many advantages for customers that AT&T believes will differentiate it. The stock has returned 22% since the start of Q4, and 17% in 2025. The company was able to expand its broadband margins in 2024 as its fiber business grew. The company now has enough fiber cable laid to support 29 million locations. This makes it a leader in this space and gives it the ability to grow substantially.  Read This Story Online Read This Story Online | I thought what happened 25 years ago was a once- in-a-lifetime event… but how wrong I was.

Because here we are, a quarter of a century later, almost to the exact day, and it's happening again. Here's the full story for you. |

| Written by Thomas Hughes

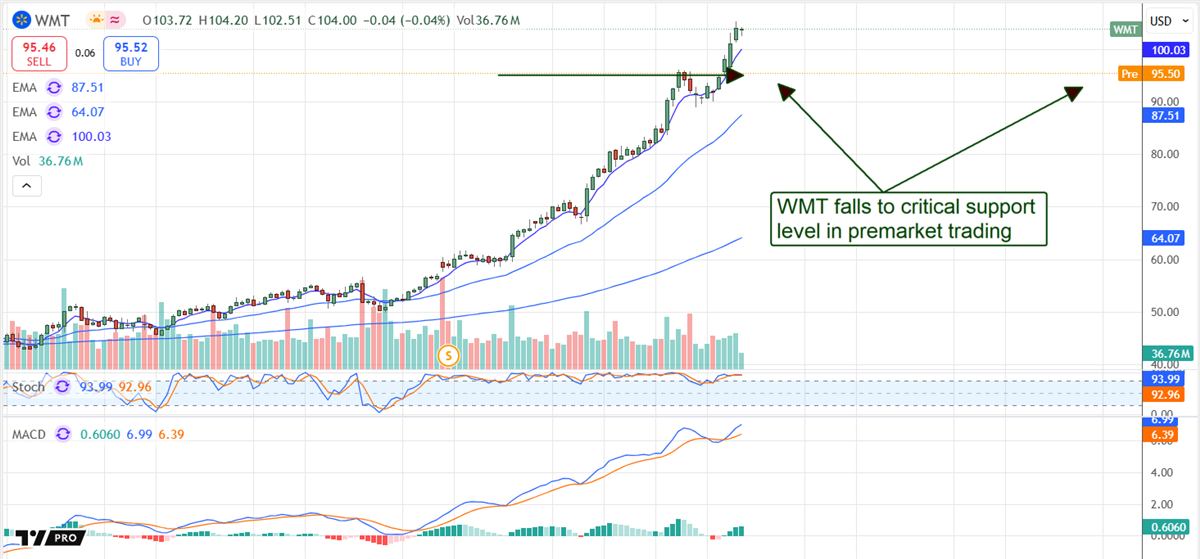

Walmart's (NYSE: WMT) February price correction is a buying signal for long-term investors. The drop is due to slowing growth and tariff fears but does little to alter the long-term outlook for earnings, cash flow, equity gains, and capital return. While slower growth and tariffs are headwinds for retailers, consumers remain strong, and the business remains solid, leaving the company to do what it does best: manage its supply chain and provide compelling value for consumers. The tariff threat is real, but it is not new. The company has been navigating a tariff-laden environment since the first Trump administration and is prepared to mitigate the impact of new tariffs to a degree. Less than 35% of the company’s products come from outside the U.S., minimizing exposure that can be further reduced through strategic sourcing and private labels. Walmart Has Strong Q4, Issues Cautious Guidance for Calender 2025 Walmart had a strong FQ4 2025/CQ4 2024 with revenue of $180.6 billion, rising by 4.1% and outpacing MarketBeat’s reported consensus by nearly 100 basis points. Critical details include strength in the core U.S. market and broad strength across categories offset by marginal weakness Internationally. Sales at Walmart U.S. rose by 5% on a 4.6% comp increase, a 2.8% increase in ticket count, and a 1.8% increase in ticket size. Sam’s Club was also strong, driven by a robust 13% increase in membership income. Sales at Sam’s rose by 5.7% on a 5.4% increase in transactions and a 1.3% increase in ticket size. The margin news is also good. The company widened its gross and operating margin to drive leveraged growth on the bottom line and outperformance relative to analysts' forecasts. The net result is $0.66 in adjusted EPS for a gain of 1000 BPS, nearly double the top-line growth, with strength expected to continue in F2026. The problem is that the guidance is weaker than forecasted but likely cautious due to consumer trends. The company forecasts only 3% to 4% revenue growth compared to the 4.2% expected by analysts, cautious because of labor market strength and retail sales data. The latest data shows persistently strong job growth, declining unemployment, and average wages rising more than 4%, underpinning a 4.2% increase in retail sales. These trends are expected to continue in F2026 and may gain momentum later in the year as Trump’s policies spur domestic activity. Walmart Capital Return Is Safe for 2025 Walmart’s investment attraction includes the capital return program. Neither the dividend distribution nor buybacks are significantly large, but together, they amount to more than 1% annualized return with shares near $100 and are sustainable. The dividend is worth less than 35% of the F2026 earnings outlook, including the 13% increase announced for the year; it yields about 0.8% and is compounded by buybacks. The buybacks reduced the count by 0.3% in 2024 and will likely reduce it by a similar amount in F2026. Regarding the balance sheet, it is as healthy as ever. At the end of F2026, the highlights include reduced cash offset by increased inventories, receivables, and assets and reduced debt. The net result is a nearly 8% increase in shareholder equity and low business leverage. The long-term debt is about 0.35X equity. Walmart Pulls Back to Critical Support Level After the guidance update, Walmart’s share price fell more than 8% in premarket trading but may not fall much further. The move put the market at a critical support level near $95, likely to trigger buying if not a rebound in action. Assuming the market confirms support at this level, Walmart’s stock will likely move sideways within a new range until later in the year. If support is not confirmed at this level, Walmart’s stock could fall to $90 or lower before hitting solid support.

Read This Story Online | |

| Written by Sam Quirke

Tesla Inc. (NASDAQ: TSLA) has had a wild ride over the past few months. In the weeks following Trump’s election victory, the stock soared 130%, reaching an all-time high in December before momentum stalled. Since then, shares have fallen more than 25%, with investors taking profits and shifting to a more cautious stance. While Tesla’s recent earnings report didn’t help sentiment, the pullback may be setting up a compelling buying opportunity. With bullish analysts calling for 45% upside, momentum swinging from the bears, and technicals improving, there are two strong reasons to buy, but also one big reason to stay on the sidelines. Reason #1 to Buy: The Sell-Off Looks Overdone Tesla’s January earnings report wasn’t pretty. Both headline figures missed estimates, and revenue growth was a disappointing 2% year over year. Given the stock’s massive rally in the months prior, this was enough to trigger a sharp sell-off as investors rushed to take profits. But the market may have overreacted. Despite missing expectations, Tesla still posted record revenue, showing that demand remains strong. Additionally, much of the disappointment is now fully priced in; shares have fallen more than 25% since earnings, creating an opportunity for long-term investors who still believe in Tesla’s growth story. Momentum also appears to be shifting back in Tesla’s favor. The RSI sits at 43 and is trending up, indicating that the stock is moving out of oversold levels. The recent downtrend could be nearing an inflection point for buyers thinking of stepping in at these levels. Reason #2 to Buy: Analysts See Big Upside Despite the post-earnings sell-off, analysts remain mostly optimistic. Just last week, Benchmark reaffirmed its Buy rating and issued a $475 price target. That echoed similar bullish calls from Stifel Nicolaus and Mizuho, which also reiterated their Buy ratings earlier this month. The price targets from the latter went as high as $515, suggesting a potential 45% upside from Wednesday’s closing price. Analysts point to Tesla’s long-term dominance in EVs and energy storage as reasons to stay bullish, even as near-term growth slows. With their sentiment remaining very much in Tesla’s favor, you can’t help but feel the recent pullback could be a great entry point before the next move higher. 1 Reason to Run: Growth Concerns Are Real The biggest reason to avoid Tesla right now is slowing revenue growth. A 2% year-over-year increase is a far cry from the double-digit expansion investors are used to seeing. If Tesla can’t reaccelerate growth in the coming quarters, it will be difficult to justify the stock holding onto last year’s massive gains. This risk has already been reflected in some bearish analyst calls. Needham & Company recently rated Tesla a Hold, and UBS Group went even further, issuing a Sell rating after January’s earnings report. Their hesitation suggests that not all of Wall Street is convinced Tesla will be able to regain its growth momentum anytime soon. Why This Might Be the Perfect Entry Point With Tesla now trading 25% off its highs, the risk-reward setup is looking more attractive. The RSI at 43 indicates that selling pressure is fading, while bullish analyst targets suggest that there’s significant room for upside. If momentum continues to shift and buyers step in, Tesla could be setting up for a strong recovery rally. But the next earnings report will be critical - if growth doesn’t improve, investors could see another wave of selling pressure. Final Thoughts Tesla’s post-earnings decline has created a major buying opportunity, but only for investors who believe in the Company’s long-term growth potential. The stock is up 10% in the past week, analyst targets suggest a lot more upside remains, and technicals indicate a possible rebound has started. However, growth concerns remain the biggest risk. If Tesla can’t deliver a strong earnings rebound, the stock may struggle to hold onto its 2023 gains. This could be a great entry point for those willing to bet on a turnaround. But for more cautious investors, it may be worth waiting until Tesla proves it can reignite growth. Read This Story Online | |

| More Stories |

| |

|

|