Ticker Reports for December 24th

5 Reasons DraftKings Stock Looks Promising in the New Year

Digital sports betting and iGaming app provider DraftKings Inc. (NASDAQ: DKNG) has been in hypergrowth mode through 2024 but continues to lose money and even issued downside guidance for 2024. The company, along with competitor FanDuel, owned by Flutter Entertainment plc (NYSE: FLUT), faces further scrutiny over anticompetitive practices. United States Senators Peter Welch and Mike Lee want the U.S. Federal Trade Commission (FTC) to investigate as they purport the two computer and technology sector companies control nearly a 90% market share of the online betting market in the United States.

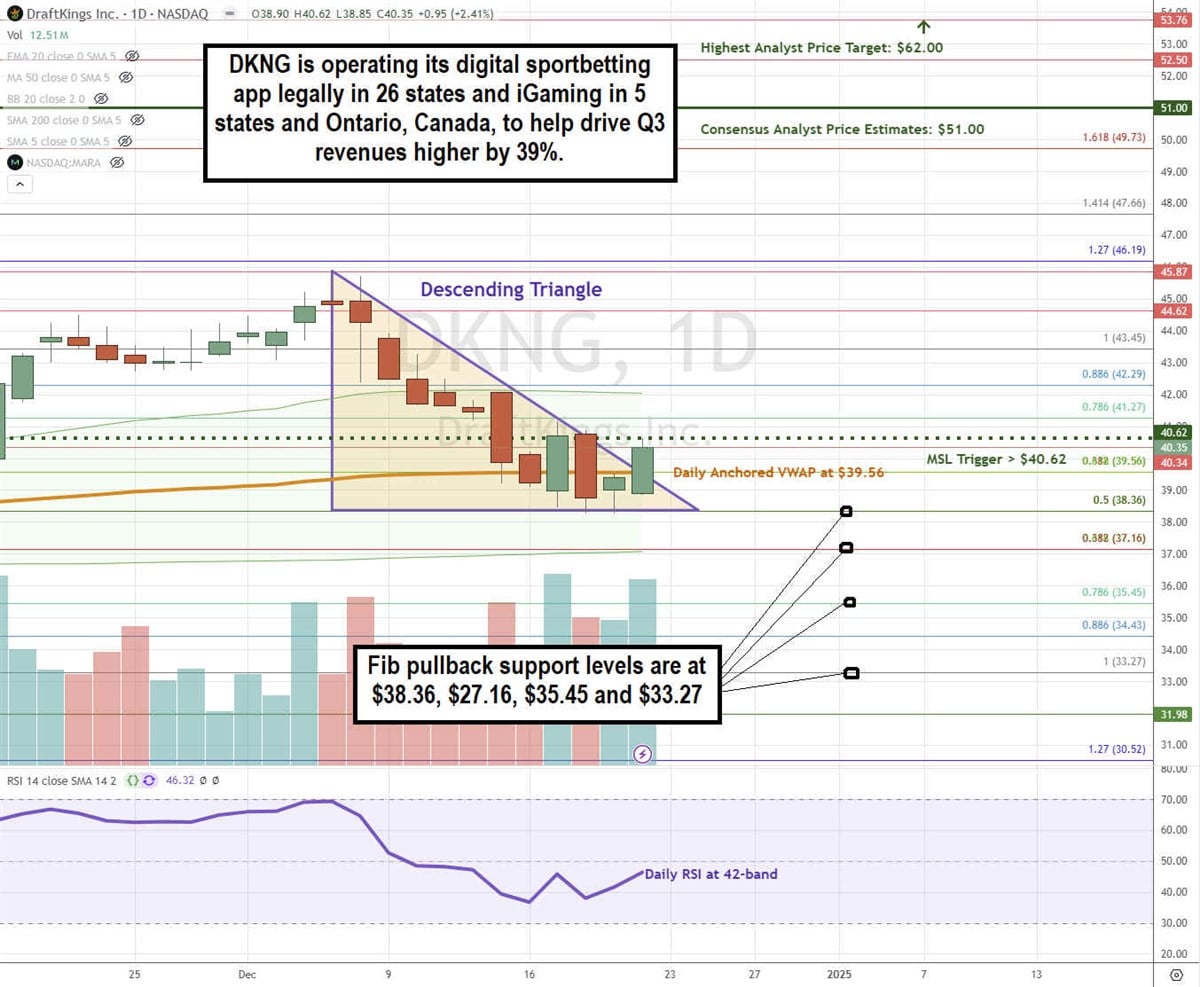

This has caused shares to sell off for seven straight sessions to its daily anchored VWAP support level at $39.56. Here are five reasons for bullish investors who have been waiting for a pullback to bet on DraftKings in 2025.

1) DraftKings Continues to Grow Revenue at Double-Digit Rates

Growth is still ongoing at DraftKings, as illustrated by the 39% YoY revenue growth in Q3 to $1.1 billion. The company has grown its monthly unique payors (MUPs) by 55% to 3.6 million. DraftKings is the third-largest sports betting platform in the United States. Its third quarter marked the return of NFL football and college football betting season. Revenue growth was driven by the efficient acquisition of new customers, healthy customer engagement, expansion into new jurisdictions, high hold percentages, and the acquisition of Jackpocket Inc., which is an app that enables users to buy lottery tickets on their mobile devices.

Jackpocket users can pick their games and numbers, which Jackpocket fulfills, and scan the ticket with an order confirmation. Tickets are stored safely in a fireproof safe. Prizes under $600 get credited to the user's Jackpocket account, while larger wins get the ticket delivered to the user. Jackpocket collects a 7% to 10% fee on the transactions as the user keeps all the winnings. Jackpocket also has live dealer and digital casino games.

2) DraftKings Will Benefit From Continued Legalization of Online Sports Betting

Online sports betting is proving to be an effective way for states to generate tax revenues. As of Dec. 21, 2024, DraftKings is currently legal and lives in 26 states (technically, 25 states and the District of Columbia) and Ontario, Canada. This represents 49% of the United States and 40% of Canada’s population. It also has in-person betting available in 14 states. DraftKings has horse racing betting in 20 states. Missouri was the latest state to legalize sports betting on Nov. 5, 2024, which DraftKings plans to launch in 2025 pending regulatory approval.

Anticipation of high for new states legalizing sports betting and iGaming. California is the largest potential market for legalizing online sports betting. However, it faces heavy opposition from tribal casinos. A previous attempt at legalization through Proposition 27 failed in 2022. Texas is the second largest potential market, but an attempt was made in 2023, but it was voted down. Florida, Georgia, and Minnesota are the next largest potential markets for DraftKings.

3) iGaming Legalization Is a Growth Driver

iGaming is the term used for online gambling through online casinos, which can include a multitude of slots, keno, digital, and live table games like blackjack, poker, and roulette. DraftKings operates only in five states, including Ontario and Canada, with its iGaming platform. While DraftKings doesn't provide specific states, iGaming margins are much higher (70% to 90%) than sports betting margins (5% to 10%). This is because the house always has an edge built into casino games along with a higher frequency of play with digital. In contrast, sports betting only offers a "vig," also called a hold, that DraftKings receives for facilitating the bets.

5) DKNG Stock Is Attempting an MSL Breakout of a Descending Triangle Pattern

A descending triangle is normally a bearish chart pattern indicator of lower highs on the bounce against flat bottom support. The descending upper trendline converges with the flat-bottom horizontal lower trendline support at the apex point. A breakdown triggers if the stock falls below the lower trendline support. A breakout triggers if the stock surges above the upper trendline resistance.

A market structure low (MSL) buy signal triggers above the high of the higher low candle following the three candle formation comprised of a low, lower low, and higher low.

After forming a swing high at $45.87, DKNG proceeded to form ten consecutive lower low candles before the higher low green candle formed above the daily anchored VWAP at $39.56. The high of the higher-low candle is $40.62, which also markets the MSL buy trigger. The descending triangle breakout can trigger if DKNG can bounce up through $40.62. The daily RSI is slowly rising through the 42-band, potentially gaining momentum. Fibonacci (Fib) pullback support levels are at $88.22, $84.35, $76.99, and $73.06.

DKNG's average consensus price target is $51.00, implying a 26.39% upside and its highest analyst price target sits at $62.00. The company has received Buy ratings from 23 analysts and Hold ratings from three. The stock has a 2.23% short interest.

Actionable Options Strategies: Bullish investors can consider using cash-secured puts at the Fib pullback support levels to buy the dip. If assigned the shares, then writing covered calls at upside Fib levels executes a wheel strategy for income opportunities while hedging the downside with the premiums received.

WARNING: "Buffett Indicator" flashing for first time in 50 years

Warren Buffett has sold a staggering $97 billion worth of stocks this year...

But why?

Our research indicates the Oracle of Omaha is quietly preparing for a historic market crash.

His most reliable crash indicator - the "Buffett indicator" - just flashed red for the first time in 25 years.

Cybersecurity Stocks: 1 Immediate Buy and 1 Dip Opportunity

Cybersecurity is a broad industry in the computer and technology sector that is comprised of many types of firms targeting different aspects of online protection. Just as home security can encompass surveillance cameras and alarm systems to panic rooms and fireproof safes, cybersecurity can entail endpoint and events monitoring to backup and data protection. Here are two cybersecurity stocks with different reactions to their earnings to present buying opportunities now and on deeper pullbacks.

SentinelOne: Protecting the Endpoints With AI

In terms of computing and cybersecurity, endpoints refer to the devices that provide access to a network that can send and receive data. Endpoints can range from desktops, laptops, and mobile devices to server and virtual machines. Hackers target endpoints to gain unauthorized access to a network and its data. SentinelOne Inc. (NYSE: S) specializes in artificial intelligence (AI)-powered autonomous endpoint protection through its Singularity Platform. It provides granular endpoint management, enabling administrators to monitor, secure, and manage devices effectively. Its AI and ML algorithms continuously learn and adapt to evolving cyber threats.

The CrowdStrike Surge That Wasn’t

SentinelOne was expected to be a major benefactor from the CrowdStrike Holdings Inc. (NASDAQ: CRWD) incident that occurred in July 2024. A software update pushed out by the company caused a widespread Microsoft Co. (NASDAQ: MSFT) Windows outage across 8.5 million devices, causing an estimated $5.4 billion in damages, including the grounding of over 700 United Airlines Holdings Inc. (NASDAQ: UAL) flights. The incident sent SentinelOne shares higher in anticipation of the mass exodus of CrowdStrike’s customers. Unfortunately for SentinelOne, that didn’t materialize, at least in Q3.

SentinelOne Misses By a Penny

For the fiscal third quarter of 2025, SentinelOne reported EPS of breakeven, which missed consensus estimates by a penny. Revenues grew 28.3% YoY to $210.6 million, beating consensus estimates of $209.73 million. Annualized recurring revenue rose 29% YoY to $859.7 million. GAAP gross margin expanded 140 bps to 74.7%. However, operating losses also grew 9.4% YoY to $89.1 million, and R&D expenses grew by 34.7% YoY to $70.4 million. There is a possibility that SentinelOne gained new customers from CrowdStrike, but the transition to their platform could take several quarters to become material. Customers with ARR over $100,000 rose 24% to 1,310. The company ended the quarter with $1.1 billion In cash and investments.

Positive FCF Causes SentinelOne to Issue Upside Guidance

The company delivered positive free cash flow for the first time on a trailing twelve-month basis, triggering SentinelOne to raise revenue growth outlook to 32% YoY for fiscal 2025.

SentinelOne issued upside FQ4 revenue guidance of $222 million versus $220.63 million consensus estimates.

Fiscal full-year 2025 revenue guidance is expected to be around $818 million, beating $815.65 million consensus estimates. Incidentally, the market reacted by selling off shares 13.2% the following day to close at $24.89. The sell-off continued for several weeks, hitting a low of $21.55, presenting an immediate buying opportunity for bullish investors.

Rubrik: Protecting the Data Ecosystem

If SentinelOne is the equivalent of a home surveillance system, then Rubrik Inc. (NYSE: RBRK) is the equivalent of a heavy-duty bank vault that protects the valuables.

The valuables, in this case, are data. Rubrik provides comprehensive data protection, management, and immutable backup services with its unique zero-trust architecture.

They specialize in cyber resilience, data archiving, recovery, and threat monitoring through its Rubrik Security Cloud platform.

Rubrik Is in Hypergrowth Mode as a Newly Minted Publicly Listed Company

Rubrik recently became a public company in April of 2024, with the stock falling to a low of $28.34 on June 17, 2024. Its recent fiscal third quarter 2025 earnings report dazzled investors and analysts, rocketing shares up to a new high of $75.79 before a pullback towards the $62.06 gap fill. The company reported a FQ3 loss of 21 cents per share, which still crushed consensus estimates by 19 cents. Revenues surged 42.6% YoY to $236.2 million, firmly beating consensus estimates of $217.5 million. Its Subscription ARR surged 38% YoY to just over $1 billion. Subscription revenue jumped 55% YoY to $221.5 million. The company ended the quarter with $632 million in cash and short-term investments.

The Growth Continues With Upside Guidance

According to consensus estimates, Rubrik expects FQ4 EPS to lose 41 cents to 37 cents versus a low of 41 cents. Revenue is expected between $231.5 million to $233.5 million versus $224.47 million consensus estimates. Fiscal full-year 2025 revenues are expected to be between $860 million and $862 million versus $834.12 million. Non-GAAP EPS loss is expected to be between $1.96 and $1.82. Rubrik partnered with flash array data storage leader Pure Storage Inc. (NYSE: PSTG) to offer companies a complete cyber resilience solution comprised of Rubrik’s Security Cloud and Pure Storage’s FlashArrayTM and FlashBlade.

Cyber Resilience Is Driving Growth

Rubrik CEO Bipul Sinha stated that cyber resilience is the number one topic in cybersecurity. Enterprises are accepting the inevitability of cyberattacks and breaches occurring. What matters the most is the ability to be resilient against attacks as well as have the capability to recover fast. Rubrik claims to deliver the fastest cyber recovery for its customers.

CEO Sinha stated, “We are the only vendor in the market that combines fast cyber recovery with data security posture management, or DSPM. We believe DSPM plus cyber recovery is the only way to deliver complete cyber resilience. In summary, enterprises are turning to Rubrik as their trusted cyber resilience partner because we can confidently meet the cyber recovery time objective or RTO.” Pullbacks on Rubrik stock back to the lower gap fill level at $54.90 present a solid pullback opportunity for bullish investors.

Blackrock's Sending THIS Crypto Higher on Purpose

It's a groundbreaking opportunity that could be poised for extraordinary gains.

The catalyst behind this surge is a massive new blockchain development…

The Next 2 AI Winners Have Triple-Digit Upside Potential

If you are looking for the next two tech winners, stocks with triple-digit upside potential that may be unlocked in 2025, look no further than SoundHound (NASDAQ: SOUN) and AppLovin (NASDAQ: APP). These companies are monetizing AI today, establishing industry-leading technology, and improving their outlooks for long-term growth in ways that analysts are noticing. The business trends are sufficient to drive their stock prices higher over time; the analysts' trends and technical chart patterns suggest that the value could be unlocked in 2025.

SoundHound Gains Traction: Hyper Growth Accelerating on Business Wins

SoundHound’s stock price rocketed in 2024 and will likely continue rising in 2025 because its hypergrowth is accelerating, and MarketBeat’s reported consensus forecast is likely to be low. Outperformance is expected. The latest results include another client win, which is important for increasing revenue and affirming business, paving the way for additional client wins in 2025.

The affirmation is important because McDonald’s is a potential client. McDonald’s scrapped its first attempt at AI-enabled call services and is reportedly reviewing SoundHound, now used in over 10,000 restaurant locations, for its more than 40,000 locations. Other restaurant chains may follow suit, and SoundHound technology is well-suited for numerous industry verticals because of how it functions. Unlike most voice recognition, which converts sound to text to meaning, SoundHound technology improves accuracy and saves time by going directly from sound to meaning.

The analysts' trends provide a strong tailwind for SoundHound stock. The consensus price target of $12 lags the market significantly but does not reflect the strength of the tailwind provided. The FQ3 2024 earnings report caused analysts at Wedbush and HC Wainwright to more than double their price targets, lifting the consensus by nearly 100% in under a week, pointing to a mid-twenty-dollar price point. The two targets average $24 or 20% above the current price action in late December, and the revision trend is expected to continue in 2025.

Sell-side interest is another strong tailwind for this market. In 2024, institutions are buying this stock at a pace double that of sellers, increasing their position to over 20%. 20% isn’t a large institutional interest, but it is growing, and with plenty of stock available, the tailwind it provides could remain in place for many quarters. Technically, the move to new highs in December is very bullish for this market and suggests a move into the $30 range is likely.

AppLovin Pull-Back Is a Buying Opportunity That Shouldn’t be Missed

AppLovin’s stock price pulled back sharply in early December when it was passed up for inclusion in the S&P 500. However, the company’s business has driven the stock price to its all-time high levels, and the S&P 500 inclusion may come later, making the pullback an attractive buying opportunity. Results in 2024 include growth in the 30% range, outperformance, and a move into the eCommerce industry expected to sustain top-line growth over the next few years. eCommerce is well-suited for AppLovin’s platform, which uses machine learning to serve ads to targeted markets.

The analysts' response to the news is as bullish as the response to SoundHound. The revisions since the Q3 report was released lifted the consensus price target by nearly 50%, leading the market to a new all-time high. The high-end range has this stock trading near $450, about 35% above the price action in late December, with revisions expected to continue rising as 2025 progresses. Takeaways from the chatter are that AppLovin will be one of the better growth stocks in 2025 as the core business remains strong and eCommerce adds incrementally to it.

Among the critical details from the price chart is the trading volume. This stock has seen its volume increase steadily for years, hitting new highs in 2024. This indicates increasing ownership, conviction, and liquidity that supports the uptrend. The uptrend in volume is due partly to institutional activity, which is ramping higher along with the share price as institutions buy on the dips. Another trend that is expected to continue in 2025.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.